Friday Speedrun: November 3, 2023

Goldilocks' Revenge

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

Here’s what you need to know about markets and macro this week

Global Macro

This week was all about yields, again. But the move was down, not up. The Treasury and the Fed did a subtle tag team on the market as they both acknowledged that rising yields are not particularly welcome and they will refrain from any action that might further panic the market.

While the supply of US Treasuries will remain yuge over the next 12 months, the signalling value of two central authorities pointing their huge government fists at rising yields has allowed the invisible hand to reverse course and stop selling bonds. While government authorities are not always successful in getting everything they want, the risk/reward of fighting them is generally bad.

They got a helping hand from the data this week, too, as ISM and nonfarm payrolls both showed softness and this obviously reduces the panic level in the market. Significant economic outperformance by the US economy is a big part of the rise in bond yields and if we are entering a softer Q4 after a red hot Q3, you can argue that yields might have peaked.

Atlanta Fed, which has been a better predictor of the US economy than economist estimates, is currently tracking at 1.2% for Q4.

Pretty much a perfect week for bond bulls as the authorities and the net of the US data generated 90 mph tailwinds.

I wrote a free piece about how to analyze soft vs. hard data this week and you can read that here.

AD

am/FX is my daily macro note that goes to a couple of thousand traders and investors. Learn more, faster. Subscribe here.

END OF AD

Stocks

The positive stock/bond correlation can be ugly when everything is going down and it can be zippy when panic subsides. This week was zippy.

The refunding announcements marked the exact bottom in stocks and the exact bottom in bonds. You can’t really say that stocks are out of the woods yet (though I think they are) because we remain in a solid down channel in the NASDAQ. A break of the October high at 15470 would change the trend back to bullish.

Note how the bull trend stayed above the moving averages, while the bear trend is chopping them like Ginsu. This suggests the move lower in stocks is corrective and the primary trend could easily revert to UP if that’s the case.

NASDAQ hourly back to May 2023 with 21day MAs

A significant bullish development is that the 200-day moving averages held like Dwayne Johnson.

NASDAQ daily with the 200-day moving averages (EMA in green and simple in blue)

You can see how the moving averages have done an excellent job of defining the trend in the NASDAQ post-COVID. A chaotic and aggressive test of a moving average followed by an impulsive rally = strong rejection.

Here is this week’s 14-word stock market summary: QRA FTW OMG. We back to bull mode.

Interest Rates

This is a chart of US 10-year interest rates on top and the bottom panel shows the difference between the current yield and the 100-hour moving average. This is a good measure of overbought and oversold and we are rather oversold to say the least. The last time yields went down this fast, venture capitalists were in tears demanding a bailout of Silicon Valley Bank.

US 10-year yield and deviation from 100-hour MA

This does not mean you need to get short bonds upon receiving this missive. It just means that we have had a big move and the risk/reward if you’re trading bonds (vs. investing in them) is to take some profit or sell puts.

In the front end, we have gone from a small chance of more hikes, and 2 cuts one year from now, to no chance of hikes and 3+ cuts by October 2024. A perfect storm of good news for bonds.

From a trading perspective, there is a useful lesson in this. Massive volume surges often mark important turning points. They are an indication of panic and forced liquidation / stop outs. The record high day in TLT (the US bond ETF) was the low.

TLT with volumes, daily back to July 2022

This isn’t hindsight, I tweeted it in real time.

https://x.com/donnelly_brent/status/1716524259000893445?s=20

This is a concept called “Volume Spike at Price Extreme.” It’s a technical observation that reflects maximum human panic / euphoria. It’s a good indicator. You can read more about it in my books.

Fiat Currencies

If I told you what happened in stocks and bonds this week, you would have been able to predict what happened in FX. The USD sold off, emerging markets ripped, and cyclical currencies outperformed. This is generally the way.

If you look at EURMXN, which is a soggy economy vs. a high carry emerging market, you will see that it tracks the VIX fairly well because when volatility is falling, carry outperforms.

EURMXN vs. VIX

There are some huge divergences between yields and FX right now and my observation is that in the long run, FX catches up to yields much more often than the other way around. For example, AUDCAD vs. rate differentials shows much higher rates as the RBA is about to hike while the Bank of Canada is done and the economy in Canada is hitting the skids.

Note how the blue line started ripping mid-October and now AUDCAD is catching up. This is called lead/lag trading and it’s a good part of a comprehensive macro toolkit. It gives you clues, not answers, but it’s a great way to find trades with positive EV.

AUDCAD (black) vs. 2-year rate differential (blue)

I like CADJPY lower because JPY is generally all about yields. Here’s CADJPY vs. the rate differential.

CADJPY vs. CA/JP 2-year differential

The path of least resistance should remain down for the USD as long as the Middle East doesn’t get worse and with the passage of Nasrallah’s speech today, it feels the world is a TINY bit less dangerous than it was yesterday.

Crypto

When criminals go to jail, it makes me hopeful. That is what happened this week as the clear-cut case against SBF played out at hyperspeed because the jury didn’t have many questions. There was also this paranoid thread on Twitter, led by Elon Musk, that SBF would not go to jail because he donated to Democrats. It’s nice to see nonsense like that emphatically disproven by the court system.

That’s a screenshot someone else took .. I didn’t retweet it FGO.

I generally stay out of the culture wars because I find both the woke and antiwoke fundamentalists to be tiresome, overconfident, and despicable much of the time, but this kind of nonsense needs to be called out as it’s an intentional attempt to destabilize what is still a (somewhat) functioning democracy, by a person some people idolize.

Anyway, the bad guy is in jail, as he should be. Now we can move on. This could be bullish for crypto as an asset class as it marks a clean close to an awful chapter for the crypto ecosystem.

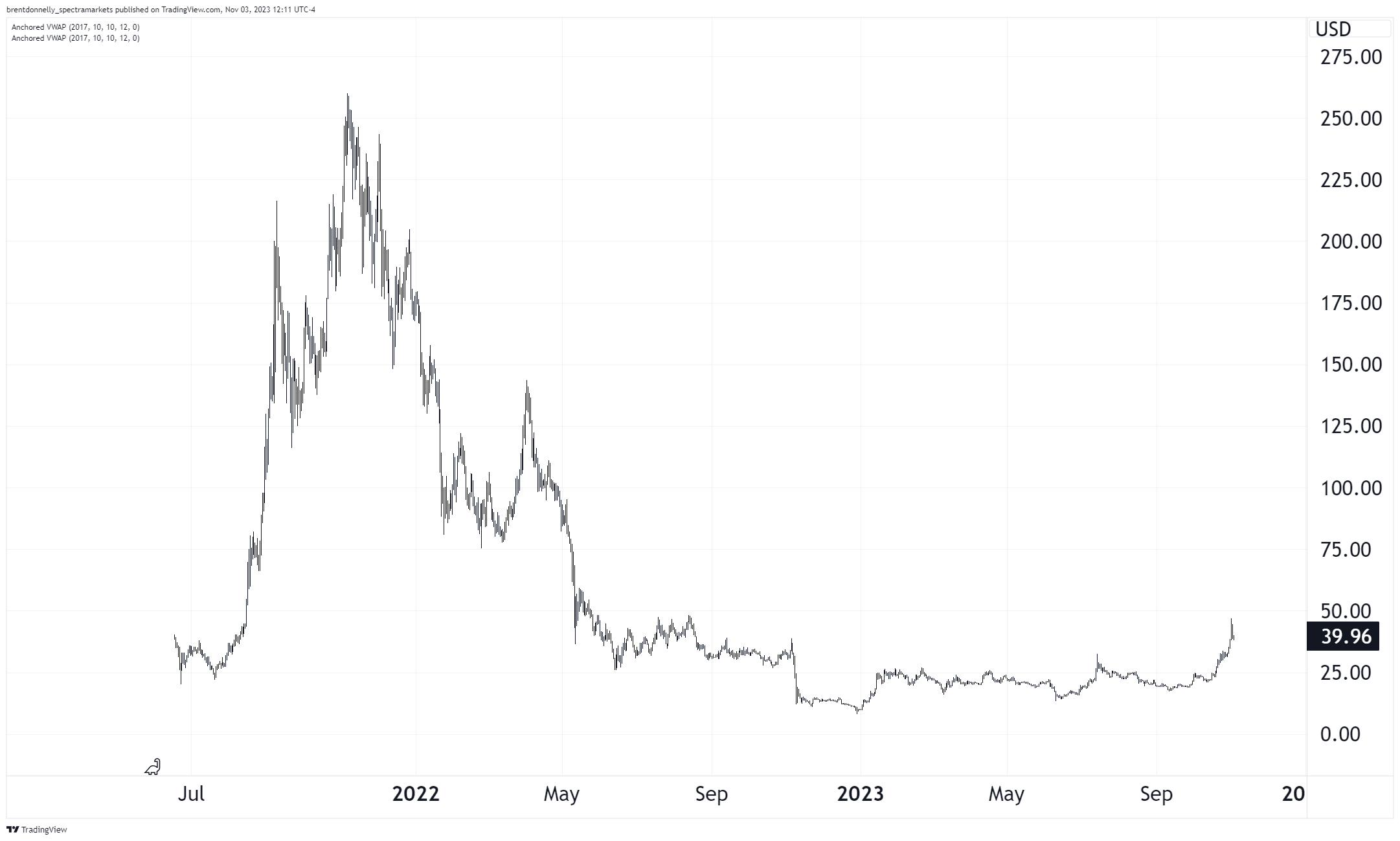

In a delicious bit of irony, SOL, the token most closely associated with SBF (other than FTT, obv) broke to new cycle highs this week.

SOLANA daily back to June 2022

Of course, if we zoom out and include Solana Summer™ it looks like this.

A 400% rally after a 97% selloff does not = ATH.

SOLANA daily back to July 2021

It’s amazing to think back to the Summer of Solana and think about just how completely fking insane the world was. Bubbles are amazing. Financial markets have no memory. Dogecoin millionaires no more.

I have a bunch of friends in crypto and they’re all seeing a meaningful pickup in activity and interest. Some of it is “buy rumor/sell fact” on the spot ETF story but some of it is a legitimate rekindling of interest.

Commodities

In a regime of falling yields, rising stock prices, and a weak dollar, you would expect commodity prices to be perky. But if that rally in risk parity is coming from economic weakness, the commodity reaction could go either way.

Oil struggled this week as the Hezbollah press conference was much more dovish than expected and specs generally trade energy from the long side again these days. It feels to me like we are settling into a period of boring equilibrium for oil prices as positioning story isn’t that significant, the bull catalysts have passed, but global growth is still OK enough to keep crude afloat.

Crude oil hourly, July 2023 to now

Same deal with gold. It found its new happy place up here near 2000 but lacks a catalyst for further acceleration. One day, it’s going to go through 2100 like a rocket but right now things aren’t bad enough to justify the move.

Despite the impact of Ozempic and GLP-1 on fast food and consumer goods stocks, it doesn’t seem to be hitting the price of sugar as there are shortage issues there and so demand isn’t the focus.

Sugar, April 2022 to now: Wedgie

OK! That was 5 minutes. Please share this Substack with any aspiring finance professionals that you know! Thanks!

Get rich or have fun trying.

Links of the week

Nerd humor

https://x.com/donnelly_brent/status/1719459082954739748?s=20

Soft vs. Hard Data

https://www.theatlantic.com/ideas/archive/2023/10/american-economy-consumer-confidence/675687/

Great commentary this week, Brent - I especially liked the commentary on crypto and $SOL. Thank you.

Always nice + helpful to end the week with this. Thank you very much