Friday Speedrun: September 22, 2023

Friday Speedrun: September 22, 2023

A huge week for macro

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

Here’s what you need to know about markets and macro this week

Global Macro

It was a huge week for global macro and markets made logical moves on the back of all the big news. Here’s a recap of the biggest events and market reactions this week.

North American exceptionalism remains in force as US Initial Claims show the US labor market remains generationally tight, high real rates support CAD, USD, and MXN, and the USD remains an all-weather currency.

Meanwhile, Europe is close to (or in) recession, the UK is suffering from stagflation and China is not as bad as people think, but still bad. There is always this idea that the Fed will hike until something breaks, but perhaps that’s another one of those pointless market truisms without a time condition like: Yield curve inversion predicts recession, or: Stability leads to instability.

I mean… Sure these things are true, but they don’t help you make money.

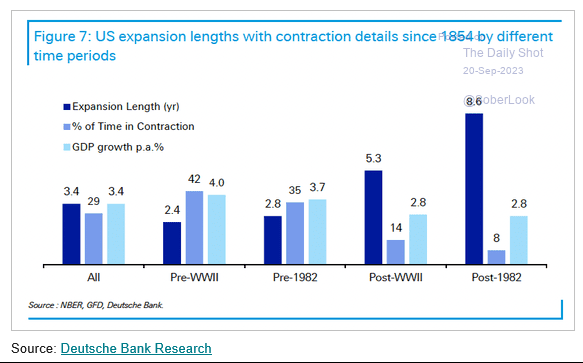

Stability and instability alternate episodically. They always have and they always will. This is especially true in the era of greater central planning from central banks as we have exchanged economic stability for financial instability. This chart from Deutsche shows how economic outcomes have been more stable over the past 40 years. We can argue over all the unintended consequences and tradeoffs. Maybe it’s been worth it, maybe not.

With so many big events now out of the way, the market has the weekend to process all this new information, and punters will be ready to place a bunch of fresh bets next week.

While US economic performance has been unbelievably exceptional, three negatives are looming.

Govt shutdown 01OCTish.

Auto strikes draining GDP

Studen loan repayments

.

Interesting point from Phil: The intriguing thing about the government shutdown is that it will likely lead to broad cancellation or delay of major US economic releases, including the October 12 CPI figure.

With a dearth of data, how can a data-dependent Fed confidently hike rates on November 1?

AD

am/FX is my daily macro note that goes to a couple of thousand traders and investors. Learn more, faster. Subscribe here.

END OF AD

Stocks

Stocks are following the script as we’re in the worst seasonal period of the year (16SEP to 09OCT) as discussed last week. The hawkish Fed and a continuing unwind of the AI bubble add fuel to the fire and we have had decent-sized moves lower this week.

Despite the big selloff, stocks have gone nowhere since June. The S&P and NASDAQ are both almost exactly where they were on June 13 (US CPI Day).

The NASDAQ range bottom is 14615/14650 as you can see in the next chart. 14650 was the gap open higher in early June and 14615 was the low in mid-August. Until we get a daily close below 14600, no real damage is done technically. Below there, it gets much uglier, fast. The equivalent level in spoos is 4328/4350.

There are 10 more trading days before the negative seasonality ends on October 9 and we revert to bullish seasonals. That’s a long time.

NASDAQ hourly back to mid-February 2023

Here is this week’s 14-word stock market summary: The calendar said stocks would fall and the Fed complied. Big support coming soon.

Interest Rates

US yields ripped higher this week while other countries saw yields move either more, or less, depending on the data and central bank action. It’s not every week that things make sense in global macro, but this week they did!

The 10-year yield chart looks like an impulsive breakout. 4.35% is the pivot.

US 10-year yields, daily 2022 to now

The following chart shows the view from 30k feet. The next big level upstairs is the 2001/2002/2006/2007 quadruple top at 5.25/5.50%.

US 10-year yields, 1989 to now

We get mostly second-tier US data next week so the focus will be more on how stocks and bonds behave and less on macro fundamentals.

Fiat Currencies

King Dollar atop his throne as US yields, a flight to safety bid on the equity selloff, US commodity export prowess, tight monetary/loose fiscal policy mix, dovish central bank meetings in the UK, Japan, and Switzerland, and weak data in Europe all show off the greenback’s all-weather nature. 2023 is another year where the dollar doomers will have to wait.

USDJPY is climbing back towards the 150.00 level, where Japan’s Ministry of Finance will itch to get involved. Yen weakness does more harm than good at this point as we have essentially doubled off the 2012 lows of 75.30. The impossible trinity concept is in play for Japan as you can only control two of three vertexes in this triangle over the medium or long run:

A dovish BOJ is going to put pressure on the yen. The MOF can smooth and push back, but they can’t change the broad direction of USDJPY, they can only cap and pray for a reversal in US yields, or normalization and rate hikes from the Bank of Japan.

Sweden is facing a similar challenge as they battle high inflation, weak growth, and a very weak currency. Tradeoffs!

Finally, GBPCAD has dropped 11 days in a row as UK policy and data contrast sharply with Canada’s continuing strong performance and sticky inflation. Global macro at its best.

Crypto

Pretty standard week in crypto. A reputed scammer got scammed and promptly received $180,000 in charity donations, while many responded he should just have fun staying poor.

https://twitter.com/BenArmstrongsX/status/1704310608395489345

Then there was a fake tweet that went viral suggesting Binance had revealed his private account balance:

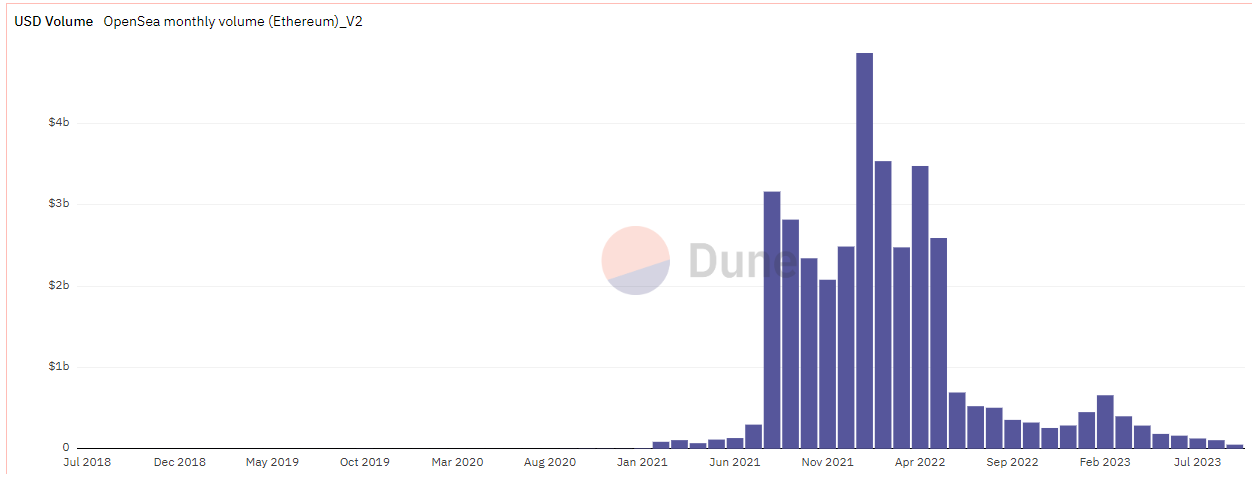

Meanwhile, NFT trading volumes are grinding back towards zero.

NFT monthly volumes transacted on OpenSea

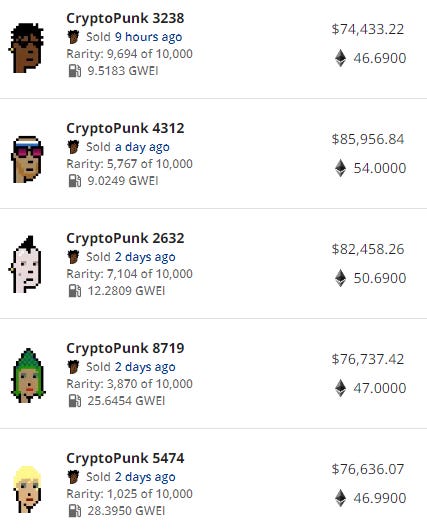

The crypto ecosystem is wild. Crypto Punks seem to be holding their value better than most other things (though I’m relying on data that could be sus) as it looks like they are still trading in the 80k USD zone while Bored Apes (remember those? LOL) are trading at 1/10th of their peak value and are half as valuable as CryptoPunks.

Recent CryptoPunk transactions from CryptoSlam.io.

Bored Ape price floor according to CoinGecko (estimated)

WAGMI frens.

Commodities

The majority of the speculative buying of NYMEX crude after Russia’s invasion of Ukraine was executed above $94.00 and the majority of the unwind of that fervor has happened below $94.00. So we have had two main equilibrium zones since February 2022: $64/$94 and $94/$130. We are almost at the top of the lower zone now.

NYMEX crude, daily back to mid-2022

The crude moves in 2022 are a great reminder of something I have seen over, and over, and over throughout my 28 years in the business. Crazy-sounding price targets are a sign of hysteria and an excellent reverse indicator. Here’s a good example of media coverage in February and March 2022.

There were similar vibes in 2008 as “experts” claimed the world had reached Peak Oil. Here’s a beauty from Barron’s:

Oil then went from $150 to $30. Lulz. Anyway, that’s just something to keep in the back of your mind next time Cathie Wood is on TV.

One last thing to think about

You can be concerned about US debt and deficits. But please remember that a chart of US debt in nominal terms means literally nothing by itself. Debt has been rising and people have been freaking out about it since 1980 or earlier.

Imagine I showed you a chart of Google’s debt. Do you conclude that Google is doomed? Or do you compare the debt and servicing cost of the debt to Google’s assets and revenue? Definitely the latter. It’s self-evident and obvious that this chart means nothing on its own. Same thing with US debt. You need to look at it in context.

Alphabet (GOOG) long-term debt outstanding

.

Yes, the US debt is large. Servicing costs look like this. They will get worse but they’re still a long way off levels seen in the 1980s.

US interest payments as a % of GDP

This chart from the CBO is menacing, but forecasting is hard and things change. But at least that chart is not just a nonsensical line going down with the caption “We are doomed!??! What is the endgame!??!”

Doomsday debt scenarios have been a thing since I was a kid. Negativity gets clicks. The doomsday scenario could be right, but 9 times out of 10, it’s wrong. Betting or investing based on doomsday scenarios is the biggest leak in finance. Pick your spots if you’re gonna bet on doomsday.

Humans adapt and respond to threats. When debt and deficits become a true threat, bond markets will freak out. That will be a scary moment and it will be a joyful (though brief) moment for the doom-and-gloom crowd. Then, central banks will intervene, governments will chill on the fiscal, and inflation will slowly erode the debt. Remember that financial markets are a political utility and the government makes the rules. E.g.:

Please click the LIKE button to receive 8 karmic jelly beans.

Alright. That was 5 minutes! You’re done.

Get rich or have fun trying.

Links of the week

Rude/funny

Forecasts without time conditions are useless, part n

https://x.com/Citrini7/status/1704366092083171445?s=20

New music from Dave, the UK grime boss

And this song reminds me of Kurt’s Unplugged version of Pennyroyal Tea. Raw.

I look forward to these every Friday!!

Brent has best commentary on markets for a weekend preparation for the week ahead, having read Brent’s excellent books, the amfx newsletter and the Friday speed run, altogether is like being mentored and coached by Brent, thanks Brent 🤜🤛