Friday Speedrun: June 2, 2023

Disinflation everywhere except stocks

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

Here’s what you need to know about markets and macro this week

Global Macro

Huge moves this week as the primary theme was disinflation. Everywhere you look, there were disinflationary signs as many factors driving prices up in 2021 and 2022 are losing momentum and new factors are emerging that should drive inflation lower. This remains to be seen but the market always shows some amount of recency bias.

German CPI, US ISM Prices Paid, Q1 Labor Costs, US Average Hourly Earnings, and South Korean CPI all gave hope that prices are going up less and less fast. Meanwhile, AI is likely to be disinflationary on a longer time horizon, and in the medium-term Amazon’s likely entry into wireless will also surely lead to lower prices. There is plenty of room for increased competition to take US mobile prices lower.

![The Cost Of Mobile Internet Around The World [Infographic]](https://substackcdn.com/image/fetch/$s_!DLzq!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F6d20f071-e80a-4a2c-a16d-e84dba3535ee_960x684.jpeg "The Cost Of Mobile Internet Around The World [Infographic]")

Inflation is not gone but it’s getting less scary. Markets are forward looking and they like what they see. Here is the Prices Paid series from the ISM Manufacturing Survey.

And German CPI:

Those janky charts were made on my phone because I am in Nashville at the Epsilon Theory Conference. If you like ET, I strongly recommend you get yourself to the conference next year. It’s the best live conference I have ever been to and it’s not all about finance. It is about how to survive and thrive and do good and communicate honestly in an increasingly polarized and fooked-up world.

How to escape from the multi-level Plato’s cave of insane media, fractured politics, and brain-damaging, addictive technology. How to escape into the real world and detect truth in a world of fiat news, intentional false narratives, and lies. I will write up all my thoughts and takeaways from Epsilon Connect in am/FX next week.

But I digress!

Rapid disinflation is the most likely path to a non-recessionary outcome in the US because as long as inflation is sticky and high, the Fed will need to keep monetary policy restrictive. The dream scenario for the tiny remaining cohort of optimists out there is that global inflation slows, the US economy stays alive thanks to strong balance sheets and a robust labor market, and the Fed eventually cuts rates not because of a massive recession but in response to inflation back at or below target. The immaculate disinflation narrative is back in play.

Every few weeks, a new macro narrative bubbles up to the surface, sits there for a bit, and then pops. We have had meaningful traction on all of the following narratives at some point this year:

US hard landing and recession

US soft landing

US no landing, acceleration

China reopening and consumption boom

China slowdown and disinflationary balance sheet recession

Inflationary boom in Germany and Europe

Recession in Germany and peak inflation

Regional bank crisis in the US may signal end of US hegemony

Fed’s gonna cut in July

Fed’s gonna hike in July

OPEC production cuts will take oil back up through the highs

OPEC doens’t matter, they have lost control of the market

US debt crisis

AI will save or kill us all

And so on.

If you’re new to global markets—this is weird. Normally, you get a few major macro narratives per year and sometimes as few as one or two. There are some sub-narratives, of course. But there I just listed fourteen stories that all have had a major impact on markets and we’re less than 42% of the way through 2023. And I could probably have listed more!

Track the 2023 progress bar here. So dumb, it’s genius.

https://twitter.com/year_progress/status/1663576018760749058?s=20

I should probably talk about the jobs data, but it was so convoluted I think I’ll pass. Not every nonfarm payrolls release contains useful information. The aggregate message from JOLTS, ADP, NFP, and Initial Claims continues to be that the US labor market is in shortage but the magnitude of that shortage gets a bit smaller each month. The numbers this week don’t change that.

If you hear someone saying “Yeah, but look at the household survey!” please refer them to this chart:

Monthly change in US jobs (household survey)

The household survey is much, much noisier than the establishment survey and often deviates wildly from reality. The establishment survey is the one people watch and talk about, and there is a reason for this. Economic data that is too noisy has no signal. That’s the case with the household survey. For more on the importance of timely, accurate, and low-noise economic data, please check out the Appendix at the end of Friday Speedrun, April 7, 2023.

AD

am/FX is my daily macro note that goes to a couple of thousand traders and investors. Learn more, faster. Subscribe here.

END OF AD

Stocks

So this week we’ve got disinflationary vibes, a strong enough US jobs market, and a massive stale short position in stocks… Excessive market positioning in one direction is like a pile of kindling with a gas can next to it. It won’t always catch fire, but if there is a spark: KABOOM. This week, we got the spark.

Sell in May and Moon in June (5-minute S&P chart)

If you would like to learn more about the importance of positioning and sentiment in markets, please check out Week 11 of “50 Trades in 50 Weeks.”

This was an interesting setup in stocks, even before the disinflationary data cascade, because at the end of last week the market seemed to believe:

A debt ceiling deal is bad for stocks because it will lead to a liquidity drain as the treasury refills its general account.

No debt ceiling deal is bad for stocks because it will lead to a crisis of confidence in US assets.

When you hear analysts discussing an important and binary catalyst, and people agree the market will go in the same direction on both of the outcomes: That’s a huge red flag. Like if you see a headline like “All roads lead to higher oil” or any other deterministic viewpoint like that… Exercise extreme caution.

Here is this week’s 14-word summary of this week’s stock market action:

Disinflation sets fire to equity shorts. China bottoms. NVDA unch. AMZN dragon slays telcos.

T-Mobile stock gaps down on possible AMZN competition

Bonds

US interest rates fell most of the week as disinflationary vibes and talk from Fed Governor Jefferson dominated until Friday.

"Skipping a rate hike at a coming meeting would allow the (Federal Open Market) Committee to see more data before making decisions about the extent of additional policy firming…”

"… a decision to hold our policy rate constant at a coming meeting should not be interpreted to mean that we have reached the peak rate for this cycle."

The next chart shows the path of 2-year yields this week. There was a violent turn back up after payrolls. The market spent the whole week betting on lower yields and took some chips off the table into the weekend.

When a trend dominates the first four days of the week, you often see a Friday reversal as traders that made money on the trend reduce their risk. Today’s yield move is a textbook example. That said, this was not just about reversing the week’s move, of course. Payrolls came out and China floated some new stimulus ideas.

US 2-year yields

Fiat Currencies

That chart of yields looks a fair bit like a chart of the dollar this week.

Dollar Index this week

USDJPY had a weird week as Japanese authorities held a meeting to discuss market moves and that included a mention of the yen. They seem to be getting a tad irritated about JPY weakness here and maybe 141 is the new 151. The Japanese Ministry of Finance intervened Hammer-of-Thor-style in USDJPY when it broke 151 last year and they have strong credibility for now because USDJPY never went back up again.

Thing is, if US yields are going up, USDJPY tends to go up, as you can see in today’s price action as yields and USDJPY recovered around half of what they lost earlier in the week. So if Japan wants lower USDJPY, they need to pray for lower US yields.

The China proxies (AUD and NZD) are back from the dead as the China narrative seems to have stabilized. Things in China are not as good as initially thought when people were fist-pumping the China reopening in January and they are not as bad as subsequently thought when people pivoted 180 degrees to “China’s screwed” last week. The truth is somewhere in the middle.

Commodities

Copper and oil had a good week, rebounding from bombed-out levels.

Copper (black bars) and NYMEX Crude Oil (blue line)

This is partly a response to the global rally in risky assets (including a huge late-week ramp higher in Asian stock markets) and the stabilization in the China outlook after some stimulus headlines. It’s also partly just mean reversion as oil continues to find strong support down in the mid-60s.

Crypto

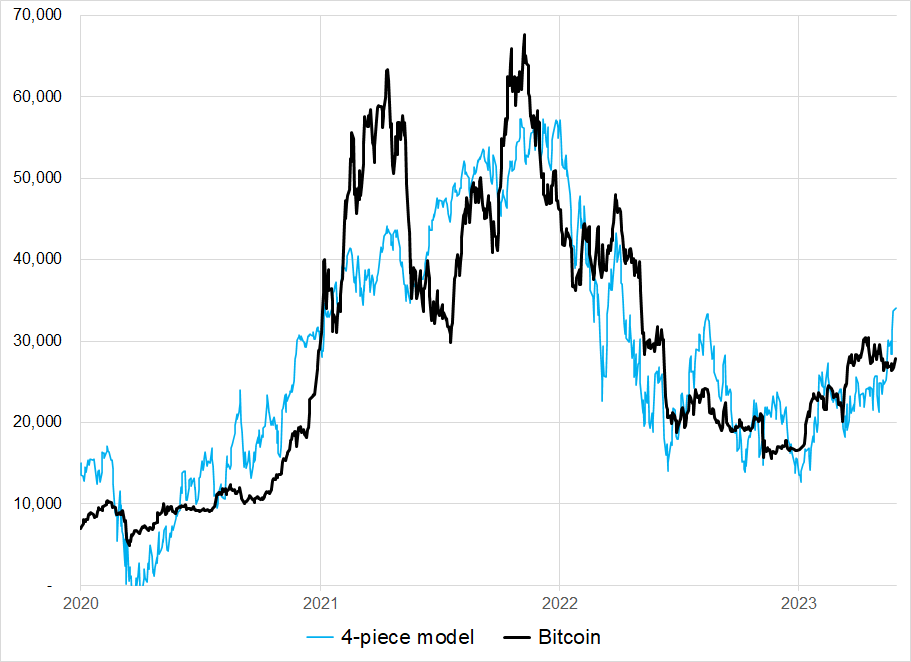

For Tuesday’s am/FX, I created a few simple models for understanding bitcoin price movements. I view bitcoin as a 4-way hybrid: it’s a risky high-tech asset, a hedge for loose monetary policy, an anti-USD proxy, and digital gold. While the NASDAQ dominates, those other inputs also matter. Here’s the model (built with 2020 to 2022 data, runs out of sample in 2023).

Correlations can change, but this is a pretty good explanation of bitcoin for now.

Simple regression of NASDAQ, US 2y, DXY, and gold vs. bitcoin

Ridiculous price targets are a red flag

On March 17, 2023, Balaji Srinivasan made a bet at the very peak of the “we’re all gonna die!” hysteria following the demise of Silicon Valley Bank. Some VCs and technofuturists (and Bill Ackman) were temporarily broken and became gripped by some sort of group insanity that led to some amazingly bad takes and perhaps the most absurd financial market prediction I have ever seen in 28 years of doing this stuff.

The bet was that bitcoin would go to 1 million in 90 days or less.

That day, bitcoin closed at 27,350. Today bitcoin is trading at 27,043. So instead of going up 4000%, it went down 1.3%. The bet was unwound on May 2, and Balaji framed it as a sort of “I lost on purpose” kind of thing. You know like when you said: “I did that on purpose!” after doing something horribly embarrassing in grade eight.

The lesson is: If someone throws out an absurd price target, run away. Absurd price targets are self-serving attempts to get clicks or attention. They are almost never genuine. They are intentionally disengenuous grabs for ears and eyeballs. This was the case in the dotcom bubble in 1999/2000 and a few times at various points during oil bull markets and it’s simply always the way. If you see a crazy price target: RUN AWAY.

https://www.fool.com/investing/2021/03/24/4-insane-assumptions-embedded-in-cathie-woods-new/

https://www.cnbc.com/2018/02/07/ark-chief-catherine-wood-sees-tesla-stock-going-to-4000.html

Balaji fans argue he just made the bet to prove a point while others argue it was a deliberate attempt to use his influence to destabilize the financial system and pump his bags. I don’t know. Maybe he doesn’t even know.

The greatest stories of all are the ones we tell ourselves.

Alright. That was 5.8 minutes. You’re done.

Get rich or have fun trying.

Links of the week

Interesting / smart / short read

If you don’t already know Epsilon Theory

https://www.epsilontheory.com/et-intro-collection/

Apple headset drops next week

https://9to5mac.com/2023/05/30/when-will-apple-release-headset/

Funny

https://twitter.com/slandrroid/status/1663571637122355202?s=20

Music

Logic. New.

Logic. Old.

https://www.stretcher.org/features/yes_yoko_ono/

Love how you manage to produce a quality piece on your phone whilst travelling, what a legend, thanks Brent!