Friday Speedrun: September 8, 2023

America is an island but Apple stock chart fugliness.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

Here’s what you need to know about markets and macro this week

Global Macro

America is a shining high-tech island rising out of a global sea of economic slurry. The US jobs data last week was OK, now Initial Claims and ISM pointed to continued strength in the US, and with oil back on the move, US yields are not far from the cycle highs again. Peak Fed is not yet guaranteed as pricing for November is still moving around.

China is slapping dozens of Band-Aids on their gaping structural economic wounds while German data is recessionary. Even Canada’s GDP data looks rather meh these days but the USA just keeps on chugging. Loose fiscal policy during an economic boom is kind of like magic.

Investment banks are cutting their US recession odds again, capitulating right as student loan repayments and a government shutdown appear on the horizon. Those two things on their own are not huge hits to GDP but they might have secondary impacts on confidence that are harder to measure. My bet is Q4 will be a slog for US growth in contrast to Q3 as a bunch of papercuts in the US and the smell of worsening conditions in China and Germany wafts over the continental USA.

Stocks

The NASDAQ is making lower highs and the up trend from March to July now looks to have rotated into a downtrend.

NASDAQ futures, February 2023 to now

A break of 16000 invalidates the view while a break of 14600 would add more evidence that the path of least resistance is now down. I will never be a permabear because that is the absolute biggest leak in finance, but I am bearish right now, mostly just on price action in AAPL, NVDA, and the NASDAQ.

These impulsive, high-velocity moves down in Apple are not the stuff of well-supported bull markets. Check out how we gapped lower in early August, sold off hard, and then filled the gap perfectly before a messy gappy thrust lower again.

Apple stock, late 2022 to now

Notice how in the up trend that started in January 2023, the pullbacks are shallow and unscary. That is no longer true. They are gappy, large, and moderately scary. Through $200, the bear view is canceled.

Here is this week’s 14-word stock market summary:

The Apple does fall far from the highs. The NASDAQ is making lower highs.

Interest Rates

We keep thinking the Fed is done. But then they’re not. This recent run of strong US data and the mildly-concerning rise in oil engineered by the cartel is putting November FOMC in play. The Fed governors have made it pretty clear they’re not hiking in September; that’s why November is the meeting that’s relevant. Market pricing has a self-fulfilling feature because the Fed tends to both guide and follow market pricing.

The y-axis label font is pretty small there. It says 45.5% chance of a November Fed hike right now. Four months ago, in May, that meeting had 100bps of CUTS priced in. Madness. Negative numbers on the y-axis are the probability of a rate cut.

It’s mind-blowing how much things move. I remember we did a macro dinner in late 2021 and we asked everyone how many 25bp hikes they expected for 2022.

Six was the massive outlier with most people expecting three or four hikes totaling 75 or 100bps. The guy that said “six” got some loud guffaws. The correct answer was 17. The Fed hiked 4.25% which is seventeen X 25bps.

Sometimes you need to have a good imagination!

Fiat Currencies

It’s been an oft-annoying year for FX traders as EURUSD, the biggest currency pair by volume, has gone nowhere while doing a stellar impression of a sine wave.

EURUSD daily chart for 2023

It looked like the USD was in trouble there for a bit in July, but nope. Loose fiscal policy + tight monetary policy is the recipe for currency strength in the US and now that the USA is also a large net exporter of energy, King Dollar has many remarkable properties:

Global reserve currency

Dominant innovator in technology draws in mega capital

Commodity currency

Safe haven in times of fear

Best growth of all the major economies

Low consumer and corporate leverage vs. most other countries, e.g.,

On the flip side, those huge deficits will matter one day, but not until the always-coming-but-never-here US recession finally hits the shore. Orthodox economics during my lifetime has always said that during times of growth, deficits should get smaller because the government doesn’t need to help the economy when she’s doing fine all on her own. The TCJA (Tax Cuts and Jobs Act) ended that orthodoxy as the Trump administration increased deficits 2017-2019 despite a strong US economy. The Biden administration has taken the baton and is now sprinting with it like Ben Johnson.

US Deficit to GDP

The huge increase in deficits right now is more like MMT than Keynes. And with rates at 5%, money ain’t free anymore—so this matters. One day. Not now.

USDJPY is going bananas again as the Bank of Japan is normalizing at a paleolithic pace and money is flowing out of Japan and into higher-yielding products abroad. Japanese authorities are warning that they will intervene again soon if the market doesn’t calm the heck down.

When the Ministry of Finance says “We are watching FX markets with urgency” that means they are getting the big USDJPY intervention machine warmed up in Tokyo. Here’s an informative but kind of insane graphic I made to show how “urgency” is code for “we're gonna intervene soon.”

The other big story in FX markets is that the super-popular FX carry trade that was basically a free money machine all year has hit a speed bump. USDMXN and EURPLN are notable as both reversed on policy announcements. Mexico’s central bank (Banxico) sent a strong message that further MXN appreciation is not welcome while the Polish central bank delivered a shock rate cut. They were expected to cut 0.25% and instead, they cut 0.75% to 6.00% in a country where inflation is still > 10%. EURPLN did this (higher EUR, weaker Polish zloty).

EURPLN hourly August 2023 to now

You may be wondering: Dude why you talking about Polish zlotys or whatever?

It may seem peripheral, but in the highly-connected global financial markets, a blowup in the carry trade can lead to other liquidations and is generally a sign that all is not safe and sound in the world. Carry blowups are a canary in the global risk appetite coalmine.

Crypto

This week’s BTC bit was guest-written by Sol Ehrlich cuz he loves the cryptos

BTC is holding a tight range after making a low at 25.2. If we take out these lows, the next important levels are 24.0 and 19.8.

24.0 is the VWAP from the November low.

Bitcoin in 2023, with VWAP anchored on the low

The logic is that people are loss averse, and will not want to sell below their breakeven price.

If this theory is wrong, and we take out these levels, then the 2017 ATH and its VWAP (19.8) represent the next strong line of support.

Coincidentally, they’re roughly the same price as each other, and the March low.

Bitcoin with two VWAPs

I should also add that I’ve seen a lot of posts saying, “We won’t go below x price/x price will happen unless there’s a Black Swan event.” Views on forecasting aside (see this post from Brent, for example, or this one from Paul Saffo), this is equivalent to saying “I’m 100% right unless I’m wrong,” and uses the hypothetical Black Swan event as a cheap way to avoid responsibility. Not to mention: There’s some sort of “Black Swan” in crypto about every three or four months.

Finally, keep an eye on the falling wedge in ETHBTC. It has been forming for about a year and falling wedges can build up a ton of energy that is released when they break out.

ETHBTC 2020 to now

And finally finally… ETF excitement keeps on building:

Commodities

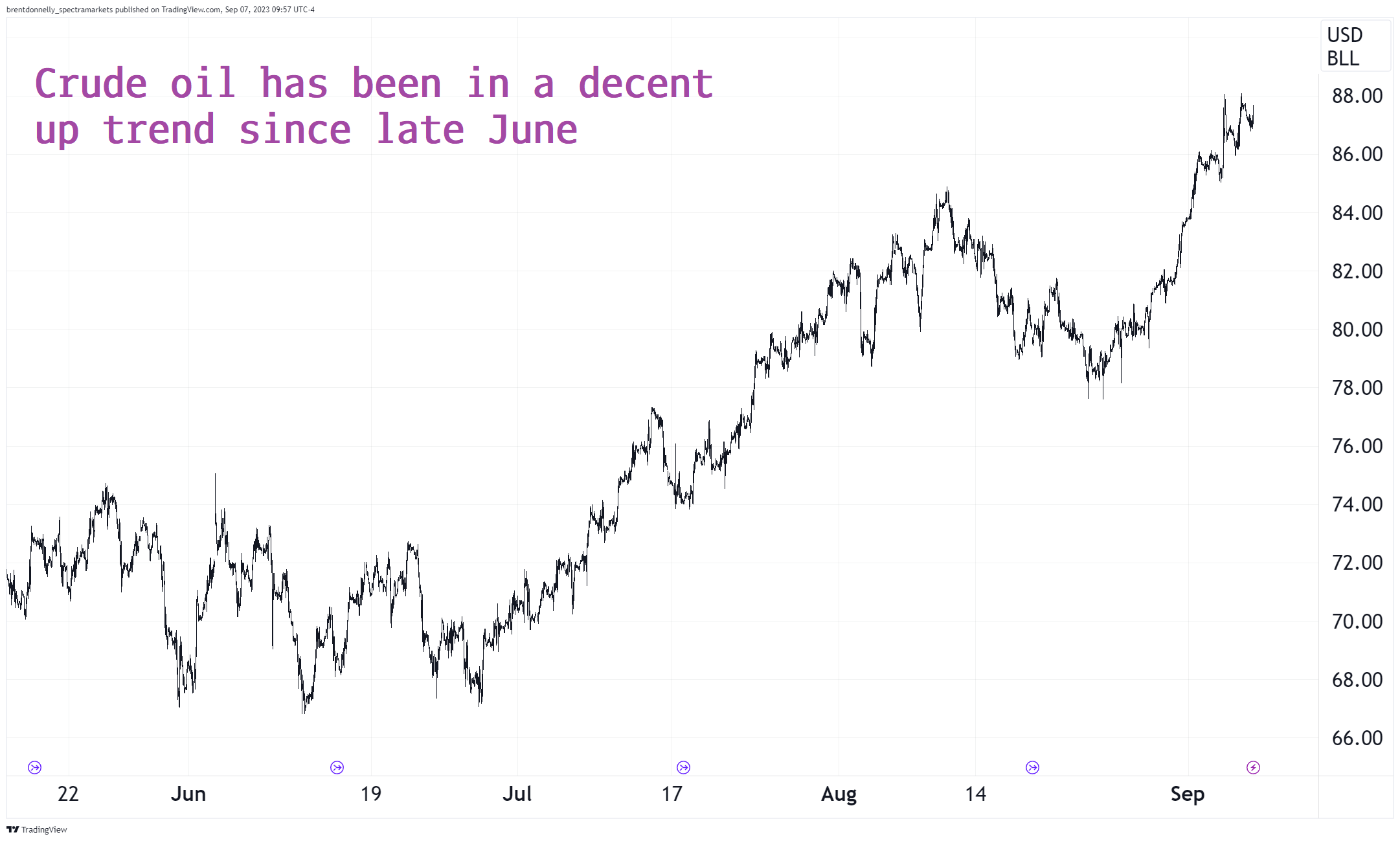

Gold and silver had a moment a few weeks ago but that moment is over and the double combo of a rising USD and high real rates in the US has capped the rally again. Oil, on the other hand, has gotten a lift as Saudi efforts to reduce production seem to be bearing fruit.

NYMEX crude oil futures, hourly chart late June to now

Alright. That was 5 minutes. You’re done.

Get rich or have fun trying.

Bits and pieces

Interesting / smart

This week’s Square Man, Round World is nice. It’s about teaching to learn.

Music

This video is Rage Against the Machine’s first concert. Scroll through and check out how the audience gathers and grows and gets into it. Awesome.

And here’s Eddie Vedder singing Better Man with his old band “Bad Radio.” He wrote the song as a teenager and the song is about his mom… So he didn’t want record it with Pearl Jam once they were famous because it was too personal.

They finally convinced him to do it for Vitalogy.

Finance nerd humor

"I'm either 100% right, or I'm wrong"

Lol.

Check out the head & shoulders on the Russell 2000.

Thanks Brent, brilliant as always.